6. May 2020

|

The automotive industry is under pressure. We are experiencing major – even disruptive – changes. The public perception of the automobile is changing and demands ecologically sustainable drivetrains. In the context of this market dynamic, electrification of the drivetrain has clearly set the stage for the public discussion and is also considered the strongest driving force in the industry. However, the sales volume for electrified vehicles is still strongly inhibited by high costs, weak infrastructure and short range. In 2016, less than 1% of all vehicles sold worldwide were primarily electrically driven. Against this background, market forecasts This market forecast focuses on the most important markets worldwide: Europe, the USA and China. It is based on a comprehensive study by FEV Consulting GmbH, which includes the following aspects:

>> THE MAJORITY OF ALL VEHICLES SOLD IN EUROPE WILL STILL HAVE A COMBUSTION ENGINE IN 2030

are certainly risky. But, despite this, an attempt has been made to assess how powertrain populations will develop in the world’s most important markets. It becomes clear that, despite the uncertainties mentioned, some reliable and central conclusions can still be made.

The CO2 limits are continually being lowered in the European, American, and Chinese markets. The level of allowable CO2 emissions, which is lower on an absolute basis in Europe and China compared to the USA, is an indication of a strong need for electrification in those two markets. The anchor points were set in 2016 (today), 2020, 2025 and 2030. By 2020, start-stop functional systems (micro hybrid) will almost completely replace traditional purely combustion engine-driven powertrains. The development of more electrified topologies is growing rapidly, relative to today’s very low sales volumes, but remains at a low level. Therefore, the sum of the market share of mild hybrids (48V), full hybrids, plug-in hybrids and battery-electric vehicles will be just over 10%. In the subsequent 5 years, a distinctive growth in mild hybrids (2025: 33% market share), plug-in hybrids (2025: 13% market share) and battery-electric vehicles (2025: 8% market share) is expected. The more distant view towards 2030 is, today, still uncertain. The interaction of the development of the plug-in hybrid market share and the sales volumes for battery-powered vehicles is not yet predictable and is primarily linked to the development progress of battery technology (energy density and price), the development of the charging infrastructure, and the development of oil prices. An additional large influence is attributed to the “zero emission zones” currently being discussed publicly. If emission-free urban zones are broadly implemented, it is to be expected that this development will strongly encourage the purchase of purely electric vehicles in cities. Irrespective of this uncertainty, the following can be safely forecast for 2030:

Market forecast for powertrain shares for Europe from 2016 to 2030 (new passenger car registrations)

When market expectations for Europe are compared to those for the USA, a divergent picture emerges, which can be summarized as follows:

These aspects lead to lower electrification rates for the market in North America, compared to Europe. Consequently, it is expected that micro hybrid drives will only be fully rolled out by 2025. Additionally, it can be assumed that by 2030, 85 to 90% of all vehicles sold will still be equipped with combustion engines. The picture that has been painted can be expanded by the additional analysis of the Chinese market.

>> IN THE USA MICRO HYBRID DRIVES WILL ONLY BE FULLY ROLLED OUT BY 2025

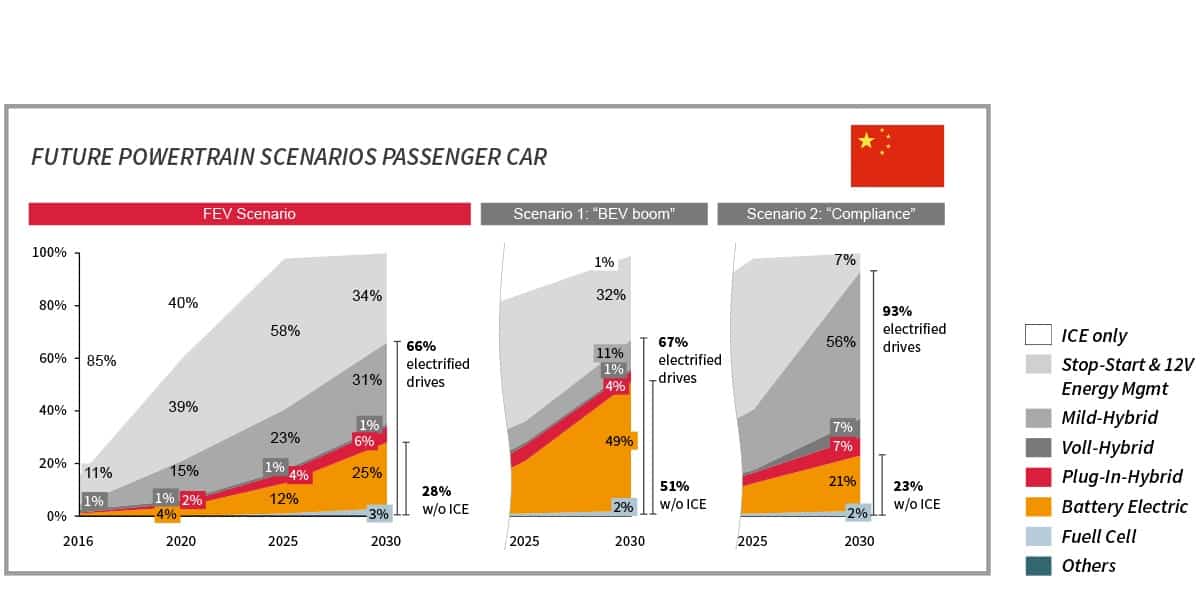

The market expectations for China relative to Europe can also be summarized as core trends:

These trends suggest a pronounced coexistence of internal combustion engine drivetrains and battery-electric vehicles in China. By 2030, only 50% to (a maximum of) 75% of all vehicles sold will have a powertrain equipped with an internal combustion engine. Concurrently, the degree of electrification of 90% of these drives will be limited to micro and mild hybrids, making the combustion engine the dominant drive unit.

In summary, it can be inferred that, even with the electrification of the powertrain increasing sharply, the majority of all drives will still be equipped with combustion engines in 2030. These combustion engines will have to work in a variety of drive topologies.

>> IN CHINA, BY 2030, ONLY 50% TO (A MAXIMUM OF) 75% OF ALL VEHICLES SOLD WILL HAVE A POWERTRAIN EQUIPPED WITH A COMBUSTION ENGINE

Market forecast for powertrain shares for China from 2016 to 2030 (new passenger car registrations)